Talk of a ramp up in Chinese government activity and strong grid expenditure data has perked up some interest that demand will perhaps not be as bad as current price weakness warrants.

Betting against policy makers ability to turn growth around hasn't really worked over the past few years. But for me it is too early to believe that what they plan to do is enough to slow the weakness already in train, with it better to wait for evidence of stabilisation in activity rather than assuming its around the corner.

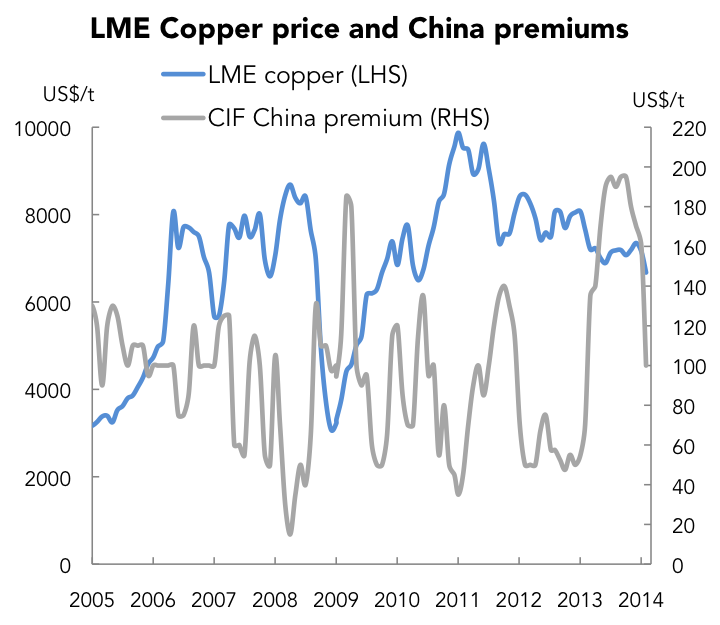

Indeed, the sell-off in copper has been more aggressive than metals like zinc and lead, suggesting the role of China in absorbing additional ex-China supply has been more important in the last 12 months or so and will continue to be so.

This contrasts starkly with nickel, where prices have rallied on supply curbs from Indonesia, although refined nickel inventories have mostly risen in the past few months.

With incremental financing demand currently weak, prices have moved lower to incentivise other buyers.

If the latest ICSG numbers are to believed, it may not be too hard to believe that additional demand can absorb the loss of financing interest. For the full year 2013, the ICSG estimates a fairly chunky preliminary deficit of 450kt when incorporating their estimates of Chinese bonded warehouses movements. That said, their data seems to assume a large destock at the start of 2013 than some of the banks do. The key question is, however, even thought the deficit is pretty big compared to a projected surplus, why have prices been falling for over a year?

A seasonal lift in activity should stop the curve from moving into contango. But the degree to which it lifts vs. last year will define how strong the spot price will be. At present the risk is that this is weak, although the balance of risks is starting to shift.