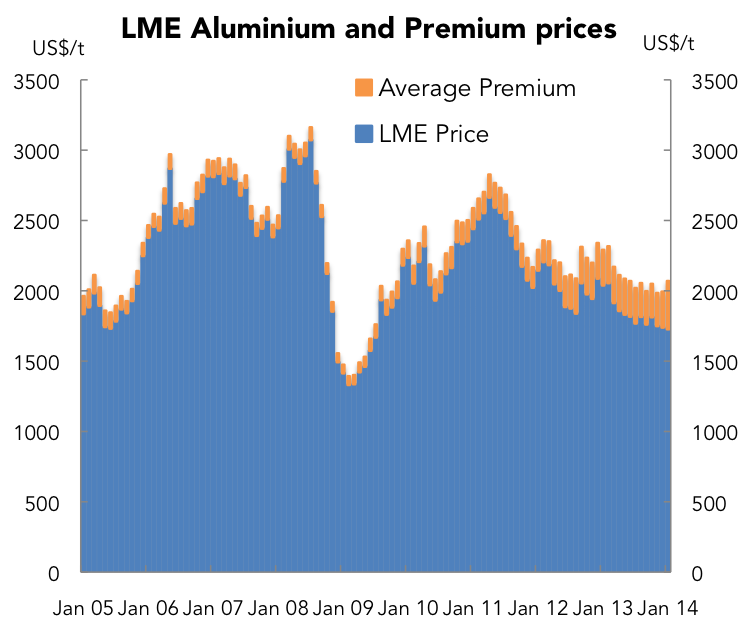

The LME's changes to warehouse rules, that will be binding next year, have yet to make a significant impact on Aluminium price spreads or premiums.

Furthermore aluminium inventories have also gone up since the last announcement from the LME, particularly at one of the "affected" warehouses of Detroit.

While some may fear this is a sign the new rules won't work, it seems more a function that the initial calculation and discharge periods don't change the status quo too much. But this will change when requirements are more stringent next year.

There are very few analysts and commentators that are not bearish on Aluminium premiums as a result of the rule changes, which are

discussed in detail in this post. In a nutshell, they should mitigate warehouse queues, which should in turn stop warehouses being able to pay cover high premiums for delivery in order to hold metal under financing deals.

But perhaps the fact that premiums haven't moved much yet is because there is still some warehouses for leeway for some warehouses to bid for metals before the first discharge period begins next year.

"Affected warehouses" with queues of more than 50 days will have to discharge the net inflow from the period 1 July 2013 to 31st of March 2014 will have to required to deliver out the additional metal over a 90 day period, on top of the 3,000 tpd required by warehouses with more than 900kt.

So there is an incentive for affected warehouses to have a no net inflow at the end of this period, to avoid this additional withdrawal requirement.

The warehouses at Vlissingen have so far seen a net inflow of 36kt during the first calculation period. So on net, they will likely looking to draw down net inventory by this amount by 31 March. But given there is still ~88 business days till then, there is still time to get metal into the warehouse and into finance deals to replace some of the cancelled warrants.

The recent experience at Detroit perhaps highlights this. Over the last 4 days, inventory here has gone up almost 90kt, which may suggest that many are not so worried about the new LME rules.

But looking back on a cumulative basis to 1 July, Detroit had seen quite a large outflow until just a few days ago. This brings net inflows into positive territory, although not drastically so at ~21kt.

To be sure, at this stage there is still the incentive to lock up Aluminium in financing deals if warehouses have leeway under the new LME rules. The cash - 3 Month contango is still steep, as it has been since mid year. Weaker Aluminium prices means that these financing deals will absorb more tonnage for the same amount of finance committed.

So while this dynamic is still in play it seems likely that Aluminium premiums will stay sticky. This is likely to change when the LME load out rules become more stringent.

This pressure will begin in the first calculation period starting 1 April 2014. This pressure arises from the requirement to load out an additional 50% of gross metal loaded in over a 90 day period.

But until then, premiums look likely to stay a bit more sticky than many may think.