Rolling Stone Magazine's Matt Taibbi is the latest journalist to take a stab at the controversy surrounding banks owning metal warehouses and commodity assets in general, with his

article available here. Taibbi brings his usual sense of outrage to anything banks are involved in, while Izabella Kaminska from FT Alphaville does a

good takedown here.

I have written about

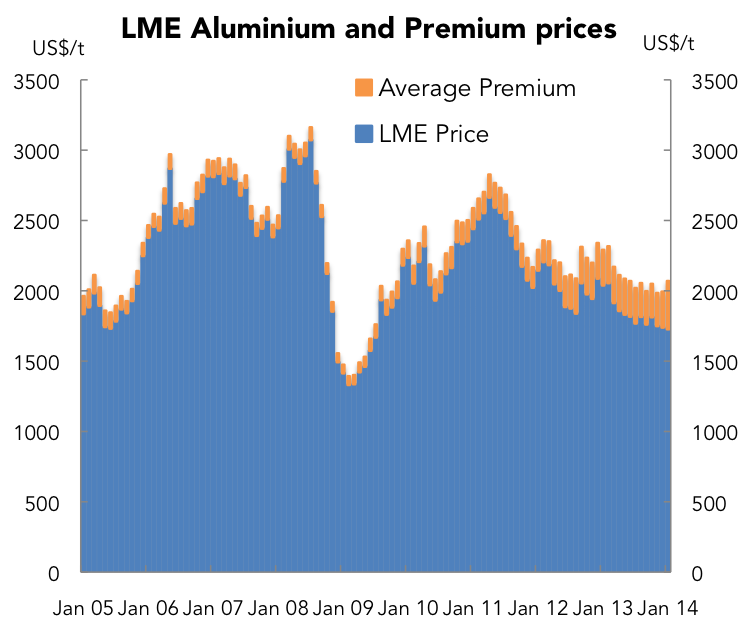

metal warehousing here, but there are a couple of points worth adding. There is not a lot of evidence to suggest that banks, or trading houses owning these assets are making metal prices high. Yes, aluminium premiums are high, but the LME price is incredibly low. Only copper and lead prices remain high from a recent historical perspective, but it would be a stretch to suggest that is due to warehousing issues given inventory is low. Even for metals where trading houses like GlencoreXstrata control a large degree of supply like zinc or nickel, prices are low.

Also, its not just owners of warehouses that benefit from rents or traders from higher premiums, but producers also capture the benefit of very high aluminium premiums. And with LME aluminium at very low levels, strong premiums are helping keeping many producers in business. The alternative to this story is the death of a large chunk of North American aluminium production.

The situation with other base metals is different to the extreme case of aluminium. Zinc does have some financing deals tying up metal in warehouses, but for copper and nickel this is not the case. The issue here is that metal has been concentrated into a few locations which are operated by Pacorini/Glencore, but this is not a riskless enterprise like financing deals are.

Finally I would add that the LME rule changes haven't affect premiums because at this stage they are not binding. That changes as of the 1st of April, when warehouses like Vlissingen and Detroit will have to load out the culmulative additional metal that have gone into these warehouses since 1 July 2013. At the moment this stands at ~230kt.

So while the rule changes won't affect incentives for financing deals, they should affect the concentration of metal in warehouses and subsequently premiums.