But one area that was surprisingly stronger was residential property markets.

These data take a little bit of work to interpret as the NBS only publish year-to-date totals. But month of month changes can be gleaned with some simple subtraction and year-on-year growth rates provide a better view of what that individual month looked like.

Some have been skeptical as to whether sales concentrated in Tier 1 cities like Beijing and Shanghai would lead to higher construction, given the lesser developed cities drive construction activity.

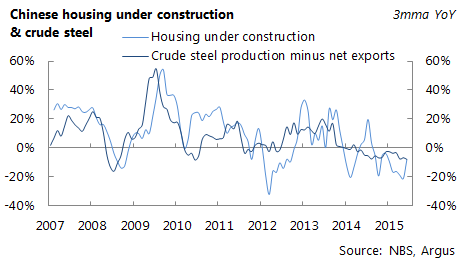

But both property starts and property under construction made the first year-on-year gain for several months in September.

One month may not make a trend, with these data tending to bounce around a lot (the chart above shows 3 month moving averages to smooth some of the changes).

But there is also good reason to think that this could be the beginning of an inflection point in demand in property markets given the drop in interest rates and rise in money and credit indicators.

A return to modest growth in Chinese property construction would be very important for many commodities. This is not just in terms of steel going into buildings, but also for consumer goods like air conditioners, washing machines and autos.

The improvement in activity also doesn't have to be particularly large to shift a given commodity price if supply is increasingly suspect given recent supply weakness and inventory is low. Metals like copper and zinc have seen the path for supply change, while met coal supply is also shrinking. Seaborne iron ore supply is still growing from major low cost producers, although this has displaced most high cost producers in seaborne markets and many Chinese producers that are increasing marginal at ~$50/t.